Imagine standing at the pharmacy counter, ready to pick up a life-changing medication, only to be hit with a $2,000 bill. It’s a nightmare scenario for anyone relying on expensive brand-name drugs. But what if you had a card that could slash that cost down to $50? That’s exactly what manufacturer copay assistance cards are designed to do. These financial tools, often called copay coupons or savings programs, are offered directly by pharmaceutical companies to help commercially insured patients afford their prescriptions.

However, these cards aren’t magic wands. They come with strict rules, hidden traps, and significant limitations that can leave you paying more than you expect later in the year. Understanding how they work-and when they don’t-is crucial for managing your healthcare budget effectively in 2026.

What Are Manufacturer Copay Assistance Cards?

Manufacturer copay assistance cards are financial aid programs created by drug makers to offset the out-of-pocket costs of specific brand-name medications. Unlike generic discounts, these cards target high-cost specialty drugs-such as biologics for autoimmune diseases or advanced treatments for chronic conditions-that often lack cheaper alternatives.

The primary goal is twofold: helping patients afford necessary care while encouraging them to choose the manufacturer’s brand over competitors or generics. According to industry data from IPD Analytics, manufacturers use these cards strategically to maintain market share, especially when facing competition from lower-cost options. For patients, this means potentially massive savings upfront, but it requires careful navigation of insurance policies.

Who Qualifies for a Copay Card?

Not everyone can use these cards. Eligibility is strictly limited to patients with private commercial insurance. If you are enrolled in government-funded programs like Medicare Part D, Medicaid, or TRICARE, you generally cannot use manufacturer copay cards. Federal regulations prohibit manufacturers from subsidizing costs for patients in these public programs to prevent anti-kickback violations.

- Eligible: Patients with private employer-sponsored health plans or individual marketplace plans.

- Ineligible: Medicare beneficiaries (Part A, B, or D), Medicaid recipients, uninsured individuals, and those covered by military health systems.

If you fall into the ineligible category, you’ll need to explore alternative options like patient assistance programs (PAPs) offered by non-profits or direct manufacturer grants, which operate under different regulatory frameworks.

How to Get and Use Your Copay Card

Getting started is straightforward, but attention to detail matters. Here’s the step-by-step process:

- Visit the Manufacturer’s Website: Go to the official site of the drug manufacturer. Look for sections labeled “Patient Support,” “Copay Savings,” or “Financial Assistance.”

- Check Eligibility: Enter your information to verify if you qualify. This usually involves confirming your insurance type and ensuring you’re not covered by a government program.

- Register and Download: Complete the registration form. You’ll receive a digital card via email or access through a secure portal. Some programs also offer printable versions.

- Presentation at Pharmacy: When filling your prescription, present the card to the pharmacist before they process your insurance. The pharmacy will submit both your insurance claim and the copay card simultaneously.

The manufacturer then reimburses the pharmacy for part or all of your copay or coinsurance. In many cases, this reduces your immediate out-of-pocket cost to zero or a nominal fee like $10-$50 per fill.

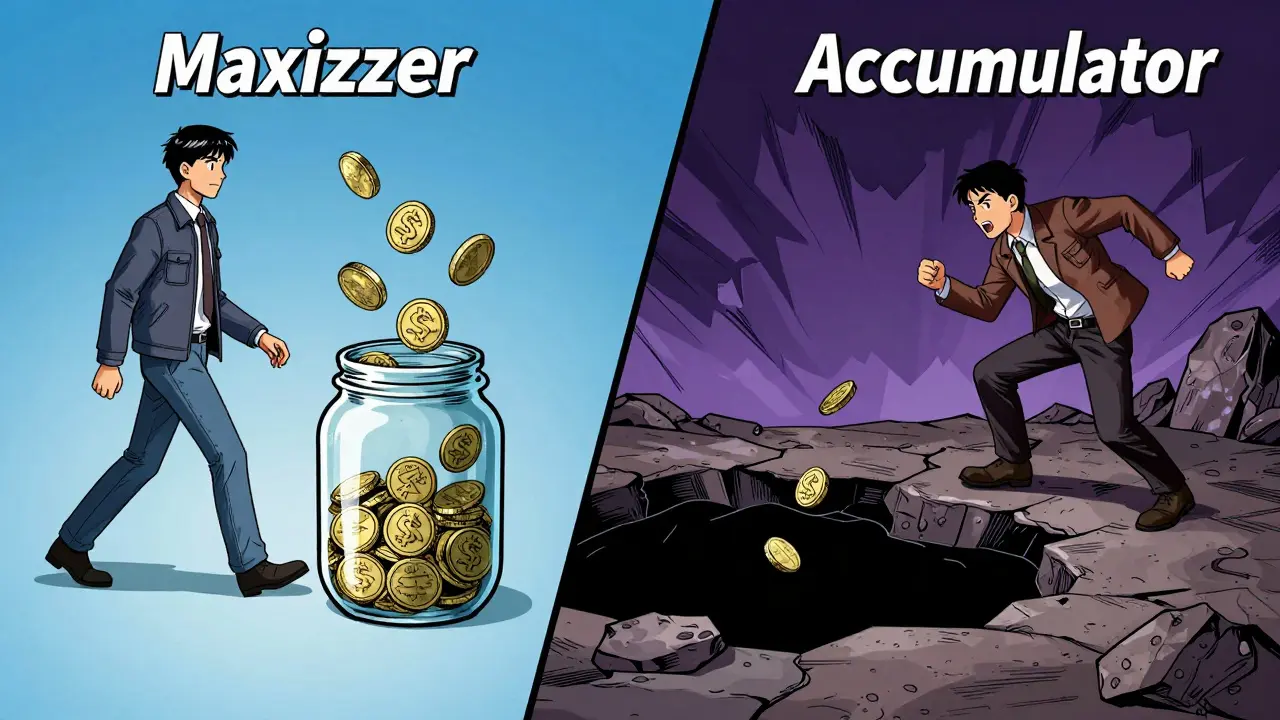

The Hidden Trap: Copay Accumulator Programs

This is where things get complicated. While the copay card lowers your immediate payment, it may not count toward your annual deductible or out-of-pocket maximum. This depends entirely on whether your insurance plan uses a copay accumulator program or a copay maximizer program.

| Program Type | How Manufacturer Payments Are Treated | Impact on Patient |

|---|---|---|

| Copay Maximizer | Counts toward deductible and out-of-pocket max | You reach catastrophic coverage faster; lower total annual spend |

| Copay Accumulator | Does NOT count toward deductible or out-of-pocket max | You pay full cost once card limit is exhausted; higher total annual spend |

As of 2023, approximately 70% of commercial health plans have adopted copay accumulator programs. This means that while you might pay $0 for the first four months of a $2,000/month medication using an $8,000 annual copay card, you could suddenly face the full $2,000 charge starting in month five because the previous payments didn’t count toward your deductible. This sudden shift can create severe financial strain.

Copay Cards vs. Pharmacy Discount Cards

If you’re unsure whether a copay card is right for you, consider comparing it to pharmacy discount cards. These third-party tools negotiate lower rates directly with pharmacies and can be used regardless of insurance status.

- Manufacturer Copay Cards: Best for brand-name specialties with private insurance. High savings potential but restricted eligibility and accumulator risks.

- Pharmacy Discount Cards: Available to everyone, including Medicare and uninsured patients. Lower savings on brand names but reliable for generics and no accumulator traps.

For example, if you’re taking a generic statin, a discount card might save you $10-$20 per fill. But for a specialty biologic costing $2,000 monthly, a copay card could save thousands-if your plan allows it.

Pro Tips to Maximize Savings and Avoid Surprises

To make the most of your copay assistance without falling into financial pitfalls, follow these practical steps:

- Know Your Plan’s Policy: Contact your insurer or check your summary of benefits to determine if they use a copay accumulator or maximizer. Ask specifically: “Do manufacturer copay contributions count toward my deductible?”

- Track Your Usage: Keep a simple spreadsheet logging each fill, the amount paid, and the remaining balance on your copay card. Most cards have annual limits (often $8,000-$10,000).

- Plan Ahead for Exhaustion: If your card has an $8,000 limit and your drug costs $2,000/month, you’ll run out after four months. Start exploring alternative funding sources-like patient assistance programs or switching plans during open enrollment-at least one month prior.

- Combine Strategies: If eligible, ask your doctor about therapeutic alternatives that may be covered better by your insurance or have lower copays without needing manufacturer cards.

Some states, like California, have passed laws requiring manufacturer assistance to count toward out-of-pocket maximums. Check your state’s regulations, as local laws may protect you from accumulator impacts even if your insurer tries to apply them.

When Copay Cards Aren’t Enough

If you exhaust your copay card funds and still face high costs, don’t panic. Several resources remain available:

- Patient Assistance Programs (PAPs): Many manufacturers offer separate grant programs for low-income patients who lose insurance coverage or exceed copay limits.

- Non-Profit Foundations: Organizations like HealthWell Foundation or PAN Foundation provide co-pay relief for specific conditions.

- Pharmacy Benefit Managers (PBMs): Sometimes PBMs can negotiate temporary caps or exceptions for hardship cases.

Contact your healthcare provider’s social worker or patient navigator-they often know which foundations support your specific condition and can help expedite applications.

Can I use a manufacturer copay card if I have Medicare?

No. Federal law prohibits pharmaceutical manufacturers from offering copay assistance to patients enrolled in Medicare Part D, Medicaid, or other government-funded health programs. Using such cards could result in penalties for both the patient and the manufacturer. Instead, look into Medicare Extra Help programs or manufacturer-specific patient assistance grants.

What happens when my copay card runs out of money?

Once the annual limit is reached (commonly $8,000-$10,000), you will be responsible for the full copay or coinsurance amount set by your insurance plan. If your plan uses a copay accumulator, you may also owe back-deductibles, leading to unexpectedly high bills. Plan ahead by tracking usage and applying for alternative assistance programs before hitting the limit.

How do I know if my insurance uses a copay accumulator?

Call your insurance provider’s member services line and ask directly: “Does my plan treat manufacturer copay assistance as counting toward my deductible and out-of-pocket maximum?” Alternatively, review your Summary of Benefits and Coverage document, though terminology varies. If unclear, request written confirmation from your insurer.

Are copay cards safe to use?

Yes, they are legitimate financial tools regulated by federal and state laws. However, always register through the official manufacturer website to avoid scams. Never share sensitive personal information like Social Security numbers unless verifying identity through secure portals provided by reputable entities.

Can I combine a copay card with a pharmacy discount card?

Generally, no. Pharmacies typically require you to choose one method of payment per transaction. Since copay cards require active commercial insurance, they usually offer greater savings for brand-name drugs. Use discount cards only if you’re ineligible for copay assistance or purchasing generics where copay cards don’t apply.